Employer Cover vs. Life Insurance Benefits

How much cover does death-in-service really provide? Is it sufficient?

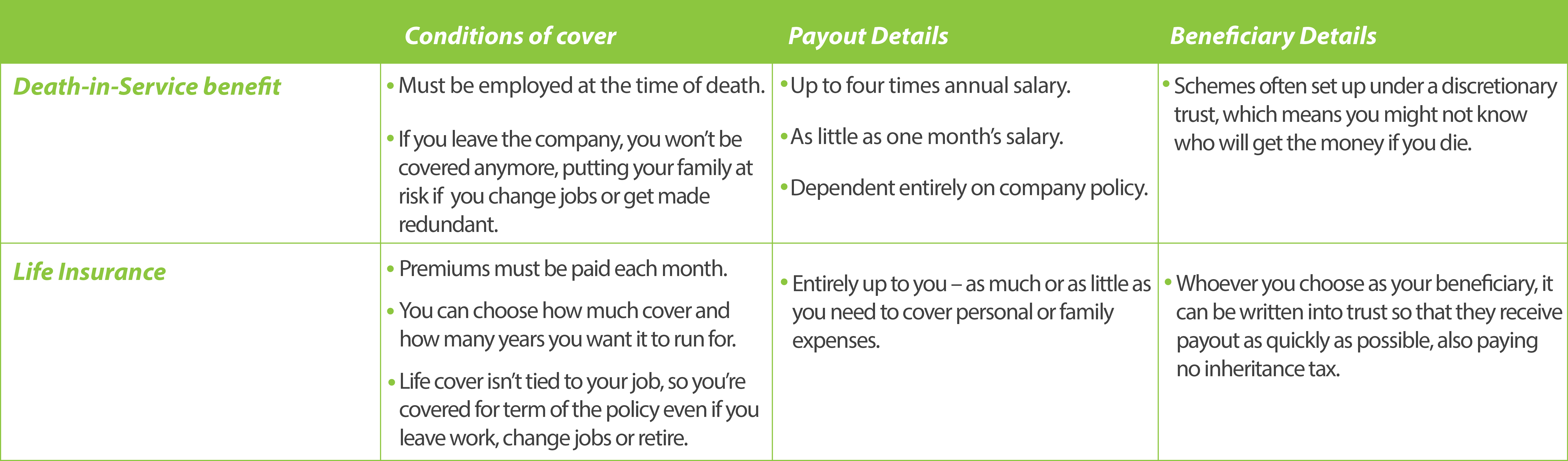

Some employers in the UK offer a type of cover akin to life insurance, known as death-in-service benefit. While there are some similarities, it’s important to know the difference between the two – here we will explain the key points you need to know.

Taking part in a death-in-service scheme should never be seen as a replacement for life insurance. Relying entirely on your employer for protection in the event of your death could lead to serious financial struggles for your family.

Death-in-service offers a lump sum payment should you die whilst in employment at the company. A common misconception is that your death must be work related – this is not the case, you must simply be on the payroll at the time you die.

In most cases, death-in-service benefit is linked to your company pension. To guarantee a payout, you must be an active member of the pension scheme when you die. By active, we mean regularly contributing the minimum pension payments.

In terms of payout size, this varies depending on the company. Some companies offer a month’s salary; others offer twice your annual salary. In the best cases, death-in-service benefit offers four times your annual salary.

This may sound like plenty, but remember – the general rule of thumb with life insurance cover is to allow for a lump sum payment ten times your annual salary. This is the amount advisors tend to recommend to accommodate all of your insurance needs.

Of course, your actual sum will vary depending on your own personal requirements, but this potential shortfall is certainly one to be aware of.

It’s also worth mentioning that death-in-service benefit would stop as soon as you no longer work for a firm – if you have no other cover, your family would be vulnerable if you were to switch jobs, get sacked, or even get made redundant through no fault of your own.

In this situation, you would be faced with buying life insurance at a later date, at an older age, maybe in poorer health – leading to higher premiums, and you missing out on the best value deal.

Separate, stand-alone life insurance policies are much more flexible than death-in-service. You are able to decide exactly how much cover you might need, as well as the length of the term and the beneficiaries.

Some death-in-service payouts go straight into a discretionary trust – meaning control of your money might not automatically go to who you want it to, straight away.

The table below shows some of the key points behind the two different types of cover. If you are unsure if your death-in-service policy provides you with enough protection, be sure to contact one of our friendly team today - an advisor will talk you through it.